Understanding Engagement Ring Insurance Cost

- Luke Zucco

- Oct 25, 2025

- 13 min read

When you start thinking about insuring an engagement ring, the first question is always the same: how much is this going to cost?

You’ll be pleasantly surprised. The cost is usually just a tiny fraction of the ring's value, typically ranging from 1% to 2% of its appraised value per year. Think of it as the price of a few fancy coffees a month to protect one of your most meaningful possessions.

What Is the Real Cost of Insuring Your Ring?

That simple 1-2% rule is the bedrock for understanding engagement ring insurance costs. It’s a straightforward calculation that cuts right through the confusion.

For example, a ring valued at $5,000 would generally cost between $50 and $100 to insure for the entire year. A $10,000 ring would fall somewhere between $100 and $200 annually. The official value of your ring is key here, which is why a proper appraisal or certification is so important. You can learn more about how that valuation works by exploring the details of the GIA certification cost.

This pricing model has stayed remarkably consistent across the globe, from the United States to the United Kingdom and Canada. While a few niche insurers might offer slightly different rates, that 1-2% range is a reliable benchmark you can count on, as noted by resources like fash.com.

To make it even clearer, let's look at some real-world numbers.

Estimated Annual Engagement Ring Insurance Cost

Here’s a quick-glance table showing what you might expect to pay based on that standard 1-2% rule for common ring values.

Ring Appraised Value | Estimated Annual Insurance Cost (1% - 2%) |

|---|---|

$3,000 | $30 - $60 |

$5,000 | $50 - $100 |

$8,000 | $80 - $160 |

$10,000 | $100 - $200 |

$15,000 | $150 - $300 |

$20,000 | $200 - $400 |

As you can see, the annual premium is a small price to pay for complete protection. It makes securing your treasured ring an accessible and practical decision. The goal here is to demystify the cost from the start and show that true peace of mind is well within reach.

What Your Insurance Policy Actually Protects

So, what are you really paying for with that annual premium? It's more than just a transaction. Think of it as a safety net for one of your most meaningful possessions, protecting not just its financial value but the sentiment behind it.

An insurance policy is designed to step in during those real-world mishaps that can turn a beautiful memory into a stressful ordeal. The best policies are comprehensive, safeguarding your ring against a whole range of unfortunate scenarios that a simple warranty would never touch.

Most high-quality policies are built on an "all-risk" foundation. This is a fancy way of saying your ring is covered against pretty much anything that could happen to it, unless a situation is specifically excluded in the fine print.

Scenarios Your Policy Typically Covers

Let’s move past the insurance jargon and get into real-life situations where a policy becomes a total lifesaver. This is where you see the true value.

Theft: You’re on your honeymoon, and someone snags your luggage with the ring inside. A good policy will cover the full cost to replace it. Simple as that.

Accidental Damage: You’re doing some gardening and whack your hand on a rock, chipping the center stone. Insurance is there to cover the repair or replacement of that damaged diamond.

Accidental Loss: This one's a heartbreaker. Maybe the ring slips off while you’re swimming in the ocean, lost to the waves forever. Your policy is designed for exactly this kind of gut-wrenching moment.

Mysterious Disappearance: This is a huge one. It’s when your ring is just… gone. You know you had it yesterday, but today it’s nowhere to be found. No dramatic story, no explanation. Many top-tier policies cover this, and the peace of mind is incredible.

A great policy reframes the engagement ring insurance cost from a recurring expense into a powerful tool for safeguarding your most cherished symbol of commitment against nearly any curveball life throws your way.

What Is Not Covered by Your Policy

It's just as important to know what your insurance doesn't cover. These exclusions are pretty standard across the industry and are there to prevent misuse.

You generally won't be covered for things like:

Gradual Wear and Tear: Over the years, the metal on your ring will naturally get scuffed and worn. This is just part of owning jewelry and is considered routine upkeep, not a sudden, insurable event.

Manufacturing Flaws: If a prong was poorly set by the jeweler from the start and the diamond falls out, that’s a craftsmanship issue. That should be handled by the jeweler's warranty, not your insurance policy.

Intentional Damage or Loss: Purposely damaging or "losing" your ring to file a claim is insurance fraud. It's illegal and, of course, never covered.

War or Nuclear Hazard: These are massive, catastrophic events that are standard exclusions in almost every insurance policy out there, from your home to your car.

Understanding both what's covered and what isn't gives you the full picture. It lets you wear your ring with confidence, knowing you’re protected from genuine accidents and life's unexpected moments.

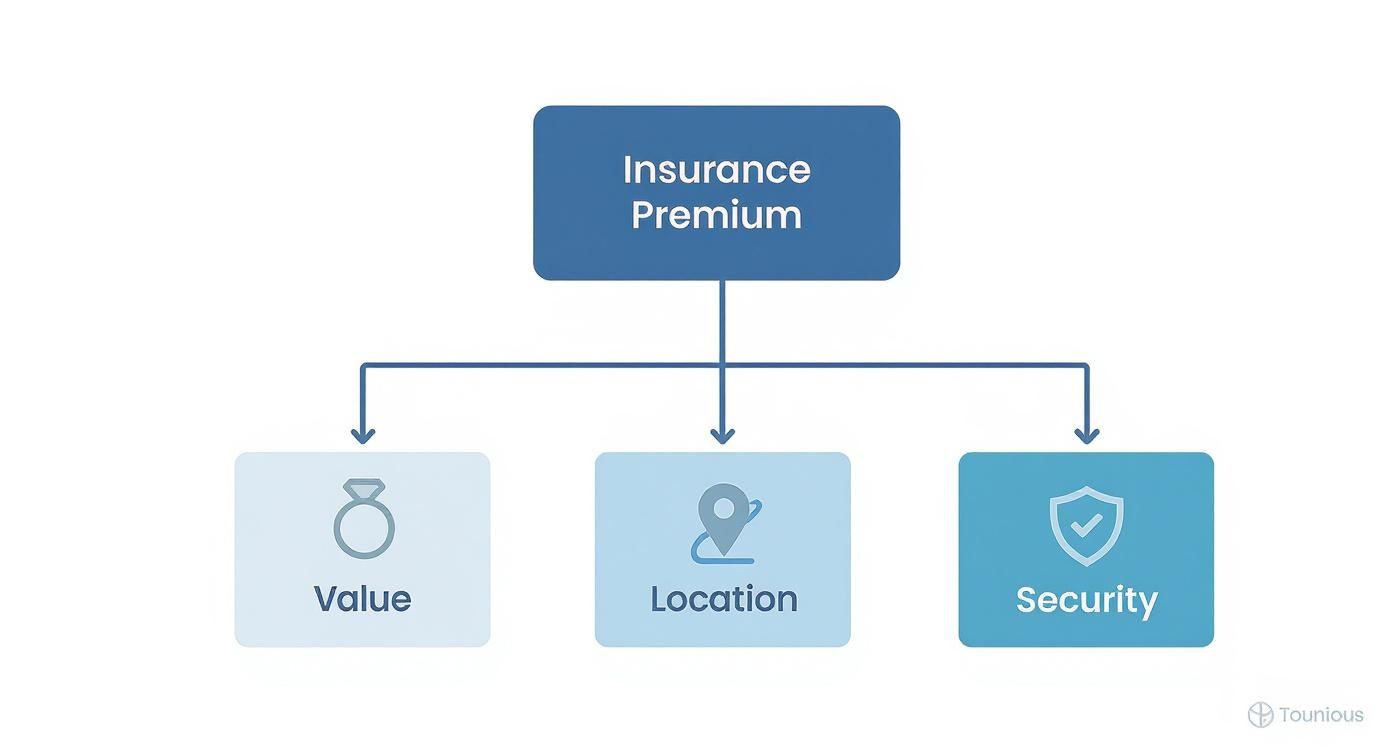

Key Factors That Shape Your Insurance Premium

That insurance quote you get isn’t a number pulled out of thin air. It’s a careful risk calculation based on a few key variables. While the 1-2% rule is a great starting point, the final cost you pay is shaped by several specific factors that underwriters look at closely.

Of course, the biggest driver is your ring’s appraised value. A more expensive ring means more financial risk for the insurer, which naturally leads to a higher premium. This is why a detailed, up-to-date appraisal is the absolute foundation of any good policy. A huge part of that value comes from the precious metal itself, so knowing how to calculate the gold value of your ring can give you a better sense of its worth.

How Location and Lifestyle Influence Cost

Where you live plays a surprisingly big role in what you’ll pay. Insurers use geographical data to assess risk, meaning someone living in a dense city with higher theft rates will likely pay more than someone in a quiet, low-crime suburb.

Your personal claim history matters, too. If you’ve filed multiple insurance claims in the past, providers might see you as a higher risk and adjust your rate accordingly.

The good news? The way you protect your ring can send a strong positive signal to insurers, often leading to some nice discounts.

Home Security Systems: A monitored alarm system is a major theft deterrent and can definitely help lower your premium.

Secure Storage: Storing your ring in a home safe or a bank’s safe deposit box when you’re not wearing it shows you're responsible, and insurers love that.

These factors all come together to create a personalized risk profile that turns a general estimate into a precise figure just for you.

Market Trends and Your Ring's Value

Broader economic trends can also have a direct impact on insurance costs. For example, recent data shows the average cost of an engagement ring in the U.S. was $6,504 in 2025. That’s down from a peak of over $9,000 in 2022, partly because lab-grown diamonds have become so popular.

A lower ring value naturally leads to a lower premium, which shows how market shifts can directly affect your bottom line. You can learn more about how these trends are changing the market on Brite.co.

Understanding these factors empowers you to see the "why" behind your quote. It’s not just about the ring’s price tag; it's about the entire context surrounding its safety and your personal circumstances.

Ultimately, your premium tells a story—one written by your ring's value, your location, and the protective measures you take. Getting a handle on these elements is crucial, and it all starts with a professional valuation. To get a better feel for that first step, check out our complete guide on how much a jewelry appraisal costs.

Choosing Your Coverage: Rider vs. Standalone Policy

When it comes to protecting your ring, you have two main paths you can take. You can add a "rider" to your existing homeowners or renters insurance policy, or you can get a standalone policy from a company that specializes in jewelry insurance.

Think of it like this: a rider is like adding a premium channel to your existing cable package. It's convenient and bundled into a bill you're already paying. A standalone policy, on the other hand, is like subscribing to a high-end streaming service designed for one specific purpose—protecting your ring with specialized, comprehensive features.

The best choice really boils down to your priorities and what you're willing to risk.

Homeowners Rider vs. Standalone Jewelry Insurance

Deciding between a convenient add-on and a dedicated policy can feel tricky. This table breaks down the key differences to help you see which option aligns better with your needs for coverage and peace of mind.

Feature | Homeowners/Renters Rider | Standalone Jewelry Policy |

|---|---|---|

Type of Coverage | Often has named perils, with gaps like "mysterious disappearance." | Typically "all-risk," covering theft, loss, damage, and disappearance. |

Claim Impact | A claim can increase your entire homeowners premium and go on your permanent record. | A claim has zero impact on your homeowners or renters insurance rates. |

Deductible | Usually tied to your primary policy's deductible, which can be high. | Often offers $0 deductible options. |

Repair/Replacement | Insurer often dictates the replacement source, sometimes forcing you to use their network. | Gives you the flexibility to work with your original jeweler for repairs. |

Best For | Lower-value rings where the convenience outweighs the potential risks. | High-value rings and anyone who wants to isolate the risk from their home insurance. |

While a rider might look easier on the surface, its limitations can create major headaches down the road. A standalone policy is built from the ground up to protect one thing perfectly: your jewelry.

The Hidden Risks of an Insurance Rider

Adding your engagement ring to a homeowners or renters policy might feel like the simplest move, but it pays to look closer. First off, many of these riders have significant coverage gaps. They often won't protect against "mysterious disappearance," which is just a formal way of saying you lost it and have no idea how—one of the most common ways rings vanish.

Even more critical is the domino effect filing a claim can have. A claim for your ring gets logged on your permanent property claim record. This can trigger a spike in your entire homeowners premium at renewal time. In some situations, multiple claims could even lead your provider to drop your home coverage completely. A relatively small claim for a ring could end up jeopardizing the insurance on your entire home.

As you can see, a high-value ring, especially in a higher-risk area, often makes a specialized policy a much smarter and more secure choice.

The Advantages of a Standalone Policy

A standalone policy is crafted from the ground up just for jewelry. These policies almost always offer comprehensive, "all-risk" coverage that includes theft, damage, loss, and that critical "mysterious disappearance," often with worldwide protection.

The real power of a standalone policy is that it isolates the risk. A claim for your lost or damaged ring will never touch the premiums or eligibility of your homeowners insurance, keeping your most important assets safely separated.

Specialized insurers also offer perks that are actually useful to jewelry owners, like the option to work with your original jeweler for repairs or replacements. Many even provide $0 deductible options, meaning you pay nothing out of pocket if you ever need to file a claim.

While the engagement ring insurance cost for a standalone policy might be slightly higher upfront, the superior coverage and financial protection it offers provide far greater long-term value and, most importantly, peace of mind.

How to Get Your Ring Insured in 4 Simple Steps

So, you've got the ring. Now, let's make sure it's protected. Getting your engagement ring insured might feel like another complicated task on your to-do list, but it's actually pretty simple.

Think of it less like a chore and more like the final step in securing a priceless symbol. Let's walk through exactly how to get it done in 4 easy steps, so you can wear that beauty with total peace of mind.

Step 1: Get a Professional Appraisal

First things first, an insurer needs to know what your ring is actually worth. This is where a professional appraisal comes in—it’s the official document that anchors your entire policy.

This isn't just a sales receipt. It's a detailed report from a certified gemologist that breaks down everything an insurance company needs to know to calculate its replacement value. Your appraisal should include:

The 4 Cs: A full rundown of the diamond's Cut, Color, Clarity, and Carat weight.

Metal Type: Confirmation of whether the band is platinum, yellow gold, white gold, or something else.

Side Stone Details: Information on any smaller diamonds or other gemstones in the setting.

Unique Markings: Any inscriptions or features that make your ring uniquely yours.

Step 2: Gather Your Key Documents

Once you have the appraisal, it's time to pull together a few other key pieces of paper. Having everything organized will make the whole process a breeze.

You'll want to have the original sales receipt, a few high-quality photos of the ring from different angles, and the diamond's grading report if you have one (like a GIA certificate). Basically, you're building a complete profile of your ring for the insurance provider.

Step 3: Compare Quotes and Policies

Now for the fun part: shopping around. Don't just take the first offer you get. Make it a point to get quotes from at least two or three different companies. Be sure to check with specialized jewelry insurers as well as your current homeowners or renters insurance provider.

When you're comparing, look past just the annual engagement ring insurance cost. The devil is always in the details. What's the deductible? Does the policy cover "mysterious disappearance" (which is a fancy way of saying you just plain lost it)? Can you go back to your original jeweler for repairs? Getting clear on these questions is a huge part of learning how to insure jewelry the right way and avoiding headaches later on.

Choosing a policy is about more than just the price. It's about finding the best value—a combination of comprehensive coverage, a fair premium, and a company you can trust to be there when you need them.

Step 4: Submit Your Application and Secure Coverage

Okay, you've picked the perfect policy. The last step is to send in your application with all the documents you gathered.

Once the insurer gives everything a final look and approves it, you’ll pay your first premium. Just like that, your ring is officially protected. You can finally wear it everywhere without that nagging little worry in the back of your mind. It's secure.

Smart Ways to Lower Your Insurance Premium

While the typical engagement ring insurance cost is already fairly affordable, there are always ways to find extra savings. With a few strategic moves, you can easily lower your annual premium without giving up an ounce of protection.

Think of it like getting a discount on your car insurance for being a safe driver. The same logic applies here. The more you can show an insurer that you're a low-risk client, the more they'll reward you with a better rate.

One of the quickest ways to shave a few dollars off your premium is by choosing a higher deductible. The deductible is simply the amount you agree to pay out-of-pocket if you need to make a claim. Bumping your deductible from $0 up to $500, for instance, will almost always lower your yearly payment. You're basically telling the insurer you're willing to handle the small stuff, and they'll thank you for it with a discount.

Proactive Steps for Bigger Savings

Beyond tweaking your policy details, taking a few proactive security measures can unlock even bigger savings. Insurers absolutely love to see that you're taking extra care to protect your investment.

Here are a few proven ways to do just that:

Invest in a Home Safe: Storing your ring in a high-quality safe when you’re not wearing it sends a strong message. It tells your insurer you take security seriously, and that simple step can often earn you a nice little discount.

Install a Security System: A monitored home security system is a huge deterrent for theft—one of the biggest risks for jewelry. Most insurance companies offer premium reductions for homes with active alarm systems.

Use a Bank Vault: For the highest level of security, keeping your ring in a safe deposit box at your bank can lead to some of the steepest discounts available on your policy.

Here's an often-overlooked tip: get your ring reappraised every few years. The market for diamonds and precious metals can fluctuate. If the value has gone down, a new appraisal could lower your ring’s insured value and, in turn, your premium.

These steps do more than just save you money; they add real layers of security for one of your most meaningful possessions. For a broader look at saving money, exploring general tips on how to reduce insurance premiums can offer even more ideas. By putting a few of these tactics into play, you can lock in great coverage at the best possible price.

Got Questions About Ring Insurance?

Alright, let's wrap this up by tackling some of the questions that pop up most often. Think of this as the final once-over to clear up any lingering doubts and get you ready to make a smart choice.

Do I Really Need Insurance If My Ring Has a Warranty?

Yes, absolutely. This is a big one, and it's easy to get them confused, but a warranty and an insurance policy are two totally different things.

A manufacturer's warranty is there to cover defects in their work—say, a prong that was set incorrectly from the start. Insurance, on the other hand, is your safety net for everything else life throws at you. It protects you from the real-world stuff: theft, accidentally losing your ring, or dropping it on a tile floor. A warranty will never cover those moments.

What Happens If I Lose My Ring While Traveling Abroad?

Great question, especially if you have a destination wedding or honeymoon planned. The answer really comes down to your specific policy.

Most specialized, standalone jewelry policies are built for this very reason and offer worldwide coverage. That means you’re just as protected on a beach in Bali as you are in your own backyard. A basic rider on a homeowners policy, however, might have geographic limits. Always, always confirm your policy's travel coverage before you pack your bags.

How Often Should I Get My Engagement Ring Reappraised?

It’s a really smart move to get your ring reappraised every two to three years. The value of gold, platinum, and diamonds isn't static; it can shift quite a bit over time.

An updated appraisal ensures your coverage actually matches your ring's current replacement value. This is key—it protects you from being underinsured if its value has gone up, or from overpaying on your premium if its value has dipped.

Is It Better to Choose a Repair or a Replacement Policy?

Honestly, the best policies don't make you choose—they give you flexibility. Ideally, you want a policy that lets you go back to your original jeweler for any repairs or to create a replacement. This is the best way to maintain the ring's specific design, quality, and sentiment.

Some policies might push you to use an insurer-approved jeweler, which can feel restrictive. It's crucial to clarify this detail before you sign anything. Look for a policy that puts you in control, whether that means choosing your own jeweler or having the option of a cash payout for the ring's full value. That way, if you ever have to make a claim, you know you'll be happy with the outcome.

At Panther De Luxe Shop, we believe the jewelry you love should be worn with confidence and joy, not worry. Explore our stunning collections of engagement rings and wedding bands, all crafted to be cherished for a lifetime.

Find your perfect piece today at https://www.pantherdeluxe.com.

Comments